The Tax Free Home Savings Account (FHSA) helps Canadians and Permanent Residents save for their first home.

The Tax Free Home Savings Account (FHSA) is a new home-buying initiative recently launched by the government of Canada as a way to save up a downpayment for first time home buyers.

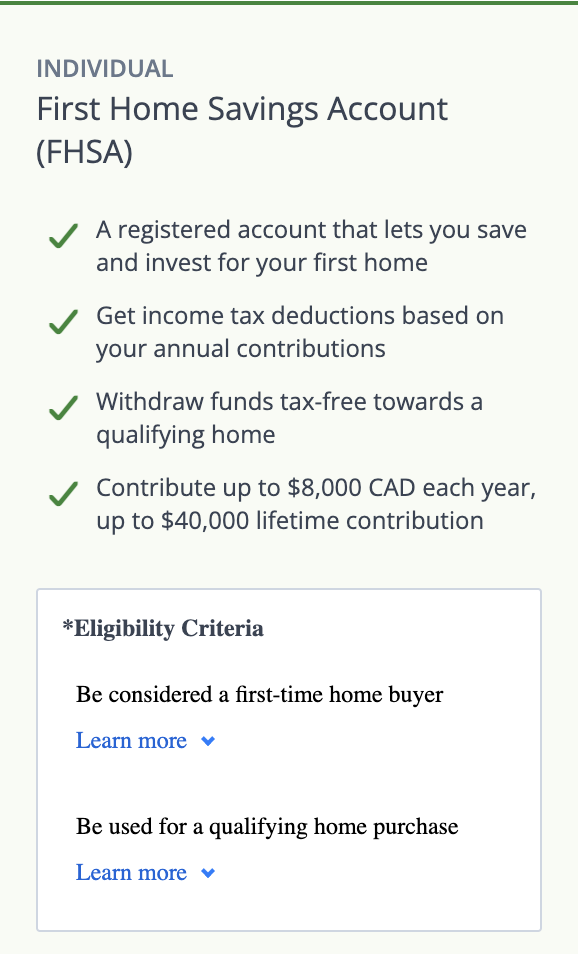

The Tax Free Home Savings Account (FHSA) combines the benefits of a TFSA and RRSP as contributions are tax deductible and withdrawals to purchase a home are tax free.

I’ve been thinking about buying an apartment since last year and was still trying to decide on my savings strategy when I discovered this opportunity through Questrade.

What is a Tax Free Home Savings Account?

The Tax Free Home Savings Account aka FHSA is a tax-sheltered account that will help eligible Canadians and Permanent Residents to save up to $40,000 towards the purchase of their first home.

The money saved in a Tax Free Home Savings Account is tax deductible. If you don’t max the contribution in any given year, you can carry it forward like you can with a TFSA and RRSP.

When, and if, the time comes to buy your home, you’ll be able to withdraw the money tax-free to buy a qualifying property.

How Does the Tax Free Home Savings Account Work?

The Tax Free Home Savings Account works by opening an account through your bank or other financial institution.

Once the account is open, you can hold investments in it which can help you reach your goals faster. You can invest in ETFs, mutual funds, Guaranteed Investment Certificates (GICs), stocks, bonds, and more.

There’s usually no minimum balance and you can invest your money in a wide range of products. The money you invest in the Tax Free Home Savings Account compounds and grows tax free.

Investment Tip – Never invest your hard earned money in anything you don’t understand.

Tax Free Home Savings Account Contribution Limits

The max you can contribute to a Tax Free Home Savings Account every year is $8,000.

If you don’t max out the account, you can carry it over to the next year up to a maximum of $8,000. The lifetime limit for the Tax Free Home Savings Account is $40,000.

The design breakdown from the government here breaks down qualifying and non-qualifying withdrawals, qualified investments, etc.

Opening a Tax Free Home Savings Account with Questrade

I opened my Tax Free Home Savings Account through Questrade and it was quite simple:-

I already have an RRSP and TFSA on Questrade so I just logged in and chose to open a new account under FHSA.

- Step 1 – Answer some account questions

- Step 2 – Sign & submit documents

- Step 3 – Fund the account

I started the account with a few hundred dollars but I’ve already worked out how I’ll be funding it every year going forward. Will I have enough money saved by the time I’m ready to buy a home?

I’m thinking between the FHSA, my savings, and the RRSP home buyers plan, I should be good on a downpayment and if I’m not, I can just roll the money into my RRSP without penalties. It’s a win-win either way.

You can get started with a First Home Savings Account (FHSA) on Questrade here. You’ll also receive a $50 trade commission rebate* after you’ve funded a new self-directed FHSA.

What is the Difference Between the FHSA and HBP (Home Buyer’s Plan)?

The handy image from Questrade below explains the differences between the First Home Savings Account and HBP (Home Buyer’s Plan):-

Tax Free Home Savings Account Rules

As great as the Tax Free Home Savings Account (FHSA) sounds, there are still a few caveats to keep in mind:-

- You must be at least 18 years old.

- You must be a Canadian or a Permanent Resident.

- You must not have owned a home at any time in the four calendar years preceding opening the account.

- The max you can contribute to the account every year is $8,000.

- You have to use the funds towards the purchase of a home within 15 years of opening the account or before you turn 71 (whichever happens earlier). If you don’t use the funds, you can roll it over into an RRSP or Registered Retirement Income Fund (RRIF) as the account will be closed. Rolling over will not affect your RRSP limits.

- You can only use the funds to buy a home in Canada.

- If you withdraw the money to buy something else other than a home, or withdraw it after closing the account, it will be taxed.

- Keep track of your contributions. Like the RRSP, if you over contribute to your FHSA, there will be a penalty.

Final Thoughts on the Tax Free Home Savings Account

This is a great way to save a downpayment on your first home and if you’re married, your partner can have an account too.

There are no immediate downsides to it. However, since this is a new initiative, the rules around it might change at any time so stay vigilant.

I will also update this article with any new rules regarding the Tax Free Home Savings Account.

You can learn more about the First Home Savings Account (FHSA) and all the accompanying rules on the Government of Canada website here.

Abi loves traveling, reading, and writing. She is a big believer in following your dreams and has been marching to the beat of her unconventional drums for a long time. She funds her adventures by making smart financial decisions and investing wisely. Her top personal finance tools include trading with Questrade, investing change on MOKA, and no-fee banking with Tangerine and Neo Financial. Learn more about Abi HERE.